The financial economy has experienced significant changes during the last few years.

Some of the most critical developments in the global financial economy have been the paradigm transitions from traditional banking to digital systems and subsequently from fiat money to digital currency.

Many well-established financial institutions have been working with unconventional Fintech companies to offer their customers improved digital services.

A recent development known as “Techfin” has joined this market and is frequently referred to as the future of the finance and banking ecosystem.

Jack Ma was the one who initially used the term Techfin. The advent of Techfin into the banking industry has spurred numerous discussions between Fintech and TechFin about the future of finance and banking.

The latest development in banking technology, known as TechFin, will soon be available worldwide. But what exactly is TechFin? What impact would this have, then?

The idea is essentially different, even if it roughly resembles the Fintech idea we have seen and grown accustomed to.

Is there a difference between Fintech and TechFin? If so, how will Fintech vs. TechFin fit into the future of finance and banking?

Before we delve into the future of finance and banking, let’s first look at the banking and financial service evolution phases.

The main products and procedures of the banking and finance industries have always been very information-intensive.

They were the first company to use information technology in their establishment to their advantage.

The first wave of banking and financial services transformation was deploying in-house essential banking solutions that included a few basic functionalities, like client data management, transactions, record keeping, etc., around the end of the 1970s.

Online banking services are made available to customers by internet-enabled institutions in the second wave of the revolution of banking and financial services.

Additionally, it led to the rise of new rivals, commonly referred to as Fintech, which was essentially internet-based platforms that used technological advancement and data power to disrupt specific financial services industry business sectors.

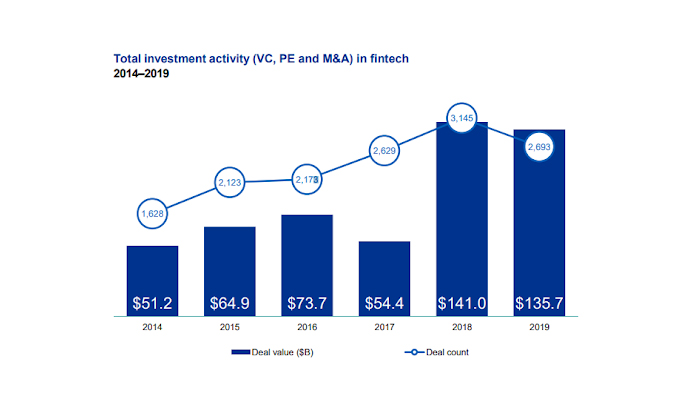

According to a report by KPMG, a total of $135.7 billion was secured by Fintech companies.

Total Investment Activity In Fintech – Image Source: Pulse Of Fintech

The third wave of banking and financial services changes is defined by integrating financial services like loans and payments into the core business offerings of non-financial enterprises.

These non-financial enterprises are known as TechFin, essentially online businesses from various industries, including eCommerce, telecommunications, search engines, social media platforms, casino companies, etc.

TechFin will bring about a significant change in financial institutions’ operations and the justification for their existence.

The financial services industry continues to be disrupted by Fintech and TechFin. We examine the differences between Fintech vs. TechFin and consider how they will affect the future of finance and banking.

Fintech (financial technology) is a general word for technology utilized to improve, modernize, digitize, or undermine conventional financial services. Fintech describes programs, formulas, and mobile and desktop applications.

Sometimes it also involves hardware, such as piggy banks with internet access. Fintech platforms enable routine chores like check deposits, money transfers between accounts, bill payments, and financial aid applications.

Additionally, they allow complex technical ideas like peer-to-peer lending and cryptocurrency exchanges.

Fintech is used by businesses to process payments, conduct eCommerce, handle accounting, and, more recently, assist with government aid programs like the Payroll Protection Program (PPP).

Even though the word “fintech” is often used to refer to technology firms that disrupt banks and financial services, financial services are the core business of fintech companies.

By identifying holes or inefficiencies in current procedures and putting emerging technology to use to fix them, a fintech company adopts a targeted strategy.

Business model innovation in the banking and financial services industry will be driven by FinTech development. Despite recent growth in their connection, banks and fintech startups still lag behind financial institutions in this regard.

What Is TechFin?

TechFin comprises companies in the technology sector whose primary business does not finance but still integrate financial services into their main offerings to enhance their appeal.

These companies aim to disrupt the banking and financial services sector by utilizing their present client connections and behavioral data. The most significant benefit of these organizations is having access to customer information.

TechFin initially concentrated on the financial services industry’s distribution side but is happy for banks to handle regulatory compliance duties. TechFin will transform the future of finance and banking in numerous ways.

They want access to customer financial transaction data since it diversifies their current customer information and gives them a complete financial picture of their users. Every technological company has specific consumer data.

While eCommerce businesses gather data on customer demand, transactions, and payment history, social media companies collect data on their customers’ social interests and activities.

In contrast to Apple and other telecommunications companies, which have information on user behavior, location, and activities, Google has data on almost every aspect of customer life.

TechFin companies are interested in adding transactional information to current client data to improve their core offering and offer supplemental financial services.

The business models used by TechFin, which focus on platforms and data, are not influenced by the margin for financial services. Banks and financial services companies, therefore, face more challenges than Fintech.

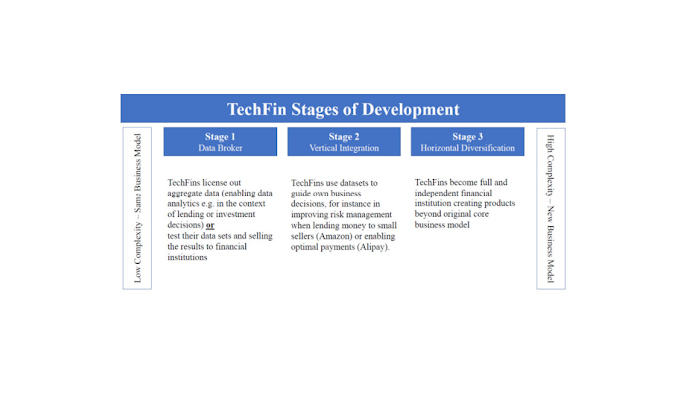

TechFin Stages of Development – Image Source: Research Gate

Fintech vs. TechFin

Despite having a similar name to Fintech, TechFin businesses primarily differ from fintech businesses in their business models and core services.

Below are some of the differences between Fintech vs. Techfin;

Differences Between Fintech vs. Techfin

TechFin uses captive client data to generate solutions, while Fintech companies lack a captive consumer base, data, or brand loyalty. On the other side, TechFin gets off to a great start with a loyal customer base and a ton of data already collected.

The variations in critical corporate goals. Another point of diversity lies within the framework of Fintech vs. TechFin’s primary business objectives.

The main goal of the fintech industry is to enhance the customer experience by utilizing digital technologies that reduce customer hassle and price while offering extra features and benefits.

Financial services are the core industry of Fintech, and profitability relies on margins.

The principal objective of TechFin’s business is to diversify into a related sector of the financial services industry to enhance its core services.

These businesses don’t solely offer financial services; unlike Fintech, their profitability is not reliant on margins.

TechFin is better positioned to work with traditional banks and financial institutions than Fintech is. TechFin is stronger than Fintech to compete with established banks and financial institutions thanks to its devoted customer base and data.

Even if it means sharing crucial data and revenue from distribution, this is not lost on the established financial services companies collaborating with internet giants.

TechFin often starts with payment solutions and adds supplemental goods and services afterward to increase revenue.

The goal of the fintech industry is to disrupt the ‘old world’ methods of financial services by maximizing the use of modern technology. Blockchain is a prime illustration of such.

Techfin’s operations aim to improve present experiences or capabilities in the financial services sector. TechFin is not as disruptive as Fintech; instead, it is more progressive.

Evaluating the Future of Finance and Banking

Fintech and Techfin have revolutionized the practice of offering top-notch financial services.

The fusion of money and technology has brought about a spectacular revolution that, in turn, has accelerated the evolution and restructuring of the banking and financial sectors.

Here’s how Fintech vs. TechFin has impacted the future of finance and banking;

1. Financial Products and Asset Classes Are Becoming More Digital

Whether used by ordinary customers, small and medium-sized businesses (SMEs), or big institutions, all financial derivatives and asset classes will be digitalized.

Traditional goods and services like stocks, government bonds, and individual banking items like payments, loans, brokerage services, and auto insurance were all part of the first wave of digitalization.

Fintech will take the lead in phase two of digitizing fund management, capital markets, mortgage markets, stock picking, SME and commercial banking, financial services, and consumer banking.

Integrating digitalization projects throughout all corporate sectors would be made more accessible by mobile applications.

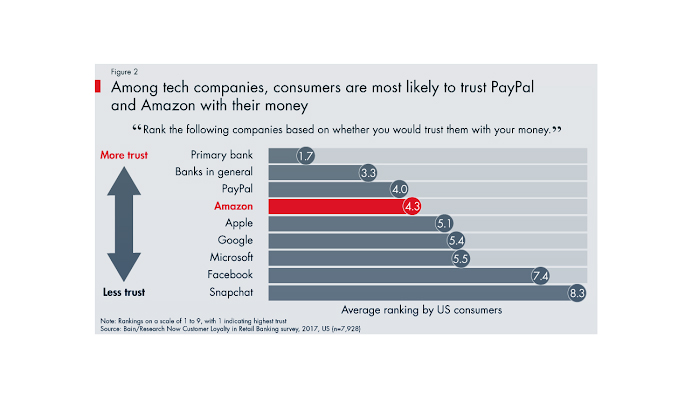

According to a study, individuals trust companies like Google, Amazon, and PayPal more than they trust the government.

Average Ranking of Techfin Companies – Image Source: Bain & Company

The business domain’s expertise and mobile application development are required for successful Fintech app development.

A seasoned mobile app development company is a good choice for a fintech or financial services enterprise looking to outsource app development.

2. Financial Services Integrated With Software and Market Solutions

The primary product and service offerings are enhanced by adding financial services, which also significantly increases the potential market for platform companies across numerous industry sectors.

Many organizations, including those who are not platform masters, will keep going to use embedded financial services.

The critical company categories in which financial services are embedded are listed below:

1. Marketplace Ecosystems

We refer to all of the activities involved in client acquisition, reactivation, and retention as part of a marketing ecosystem. B2C markets, eCommerce support systems, and B2B marketplaces with a vertical focus all fall under this category. This group comprises companies like Amazon, Shopify, and others.

2. Vertical Software Providers

Are incorporating payments into larger software packages emphasizing corporate operations and customer interactions, such as content management systems, point-of-sale systems, and hospital administration systems.

The education, hospitality, and healthcare sectors can benefit from the capabilities that make up the software suite known as Flywire. These have specific payment criteria that parallel platforms cannot fulfill.

3. Business-to-Business (Workflow Systems)

Automate purchasing, travel and expenditure reporting, and treasury management all impact the future of finance and banking.

Native payment solutions give users easy backend reconciliation and delivery, hastening the shift of B2B market divisions to digital payments.

The United States Fintech market is anticipated to have positive growth and is projected to expand at a CAGR of 10.1% over the following five years (2021-2027).

Due to increasing investment and the number of transactions in the US, the Fintech vs. Techfin business is rising.

Examples of TechFin Companies

TechFin Companies Concept – Image Source: Medium

Fintechs, banks, and other financial institutions find it difficult to compete with most TechFin enterprises due to their sophisticated backend technology.

Several businesses have jumped on the TechFin bandwagon, including:

1. Amazon

One of the first businesses to utilize the new TechFin capabilities was Amazon.

Providing numerous financial services through its application has improved the consumer experience. Customers can use Amazon Cash to add money to their Amazon Balance.

Customers can also pay for goods and services with Amazon Pay. It provides loans to small and medium-sized businesses and plans to offer to check accounts to its clients by working with big banks.

Shop With Amazon Pay – Image Source: Amazon

2. Google

Google launched Google Pay, a tool that enables people to sign up using their Google accounts.

Users of Google Pay can use the app to pay for goods and services and make payments to one another.

3. Apple

Users of iMessage can send money to other iMessage users.

Using Apple Cash – Image Source: Apple Inc.

4. Rakuten

About 2 million subscribers of the Japanese texting service Rakuten. It is more than just a texting app, though.

Additionally, it offers its members credit cards, security services, and mortgages. It is regarded as one of the biggest Japanese internet shopping marketplaces.

5. Alibaba

Jack Ma, the Chinese company’s owner, is the brains behind TechFin.

Alibaba recently dipped its toes into the financial industry by providing loans, investment services, and payment solutions to its users based on their website usage history.

Examples of Fintech Companies

By 2025, McKinsey projects that global payments will total $2.5 trillion. Payments are a prime industry for Fintech vs. Techfin to target for innovation and disruption due to their wide range of potential.

Numerous diverse fintech businesses provide their customers with outstanding services. Here are a few well-known instances of companies looking to improve the future of finance and banking using Fintech;

1. Klarna

Providing payment services for eCommerce and, more broadly, any activity involving a digital transaction, Klarna is a fintech startup.

In particular, Klarna offers installment plans, pay-after-delivery choices, direct payments, and payments for online stores. It is an advantage to the future of finance and banking.

Customers can use the service’s licensed bank to make purchases using the “buy now, pay later” principle. Products can be bought using interest-free or inexpensive installment plans.

By dividing a transaction in this fashion, customers can pay for goods gradually rather than all together at once.

2. Robinhood

Several apps, including Robinhood, enable online stock trading by condensing the typical broker-client relationship into a simple-to-use online interface.

Even though trading doesn’t cost much, Robinhood’s founders saw that most investment platforms charged exorbitant fees to their clients.

The company’s fee-free trading platform was introduced in response, enabling mobile phone users to trade stocks more effectively.

The business provides commission-free stock trading and exchange-traded funds, and most recently, it has begun giving cryptocurrency trading to its subscribers.

Since its inception in 2011, Stripe has assisted companies of all sizes with processing online payments, obtaining business financing, and automatically calculating and collecting sales taxes.

In 2018, Stripe handled $640 billion in payments, up 60% from 2020.

4. Venmo

One well-known P2P payment tool is Venmo, which enables users to conduct transactions swiftly via direct digital file-sharing.

People can efficiently complete free transactions with their loved ones or low-fee payments to companies thanks to services like Venmo.

The company’s most notable feature is how it presents its transactions in a social stream, enabling customers to share and show payments with friends.

Through social networking and smart devices, services like Venmo have benefited from a society that is becoming more cashless.

Venmo Payment Tool – Image Source: Venmo

5. Square

Businesses can now approve credit cards on a smartphone, tablet, or terminal, thanks to Square, a point of sale and payment service.

Before firms like Square, small businesses occasionally struggled to accept credit cards because of exorbitant rates and complicated technology.

Companies can collect payments, issue receipts, and give clients virtual gift cards thanks to Square’s simple-to-use process.

Is Techfin the Future of Finance and Banking?

The TechFin dynamos will undoubtedly put the capabilities of legacy financial organizations to compete in the future banking ecosystem to the test.

The enormous technology firms, made up of digital platforms, are influential and have also discovered ways to cut operating expenses and monetize their business models.

We know that most tech behemoths have the digital know-how, the sizeable client base, and the freedom to expand their corporate brands into banking.

Furthermore, some of these businesses generate a level of confidence formerly reserved for conventional banks and credit unions.

Consumers are increasingly likely to adopt financial products given by non-traditional institutions if the experience is better than legacy organizations. Notably, this is accurate. It is especially valid for younger clients who have grown up on digital devices.

Since consumers primarily desire a better and more dependable UX (user experience) and design for their merchandise and services, Techfin’s success rate of advancement and strategy may inevitably be slower but more substantial.

Final Thoughts

Fintech provides a novel financial solution or process based on technical possibilities in a new product or service style to address a specific financial service issue for customers.

TechFins include various current financial and technology solutions into its business model. Both fintech and TechFin are upsetting forces in the future of finance and banking.

Traditional institutions must instantly digitize their corporate entities if they hope to thrive in the digital revolution.

The financial economy itself holds the key to where finance will go in the future. The truth is that Fintech vs. TechFin companies will eventually merge, and their solutions will become comparable in the future of finance and banking.

Additionally, the combination of unconscious caution and a fluid user experience can only be realized once Fintech becomes TechFin. Whether the merger occurs, the banking sector will evolve, and Fintech vs. TechFin transformation is inevitable.

Acodez is a renowned web development company and web application company in India. We offer allkinds of web design and Mobile app development services to our clients using the latest technologies. We are also a leadingdigital marketing agency in India, providing SEO, SMM, SEM and Inbound marketing service at affordable prices. For further information, please contact us.

Looking for a good team

for your next project?

Contact us and we'll give you a preliminary free consultation on the web & mobile strategy that'd suit your needs best.

Rithesh Raghavan, Co-Founder, and Director at Acodez IT Solutions, who has a rich experience of 16+ years in IT & Digital Marketing. Between his busy schedule, whenever he finds the time he writes up his thoughts on the latest trends and developments in the world of IT and software development. All thanks to his master brain behind the gleaming success of Acodez.