The financial industry is at the crossroads of transformation in an era of rapid technological advancement and ever-evolving customer demands.

At the heart of this revolution lies Banking as a Service (BaaS), a disruptive concept rewriting the traditional banking playbook. Its market size reached $ 637.40 Billion in 2022 and is projected to soar to an astonishing $6,943.49 Billion boasting an impressive CAGR of 32.9% from 2024 to 2030.

BaaS represents a paradigm shift, enabling non-bank entities to harness the power of banking functionalities and seamlessly integrate them into their own offerings.

Fintech startups, technology giants, and even e-commerce platforms are embracing this innovative approach, empowering consumers with unparalleled access to diverse financial products and services.

Join us on a captivating journey into the heart of BaaS, where you’ll explore its significance as a game-changer, real-world examples, and its myriad benefits. We will also look at the future of BaaS.

Banking as a Service represents a remarkable technological advancement, allowing non-bank companies to offer financial services to their customers without the need to build an entire banking infrastructure from scratch.

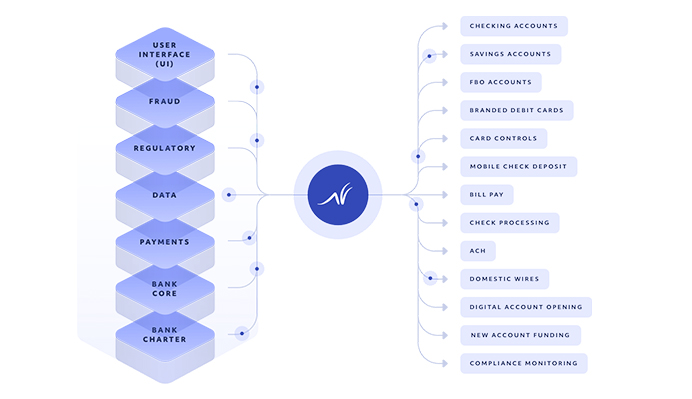

This concept emerged due to the growing demand for accessible, innovative financial solutions. The heart of BaaS lies in its application programming interfaces (APIs) that enable seamless communication and integration between various systems.

Through these APIs, non-bank entities, such as fintech startups, e-commerce platforms, and even other banks, gain access to essential banking functionalities like payments, lending, and account services.

BaaS APIs Solutions – Image Source: Grasshopper Bank

In 1997, Sumitomo Bank launched the first online banking service. But, it was only in the 2000s that online banking gained widespread adoption. For instance, around 32% of people in the UK used online banking services in 2007, skyrocketing to over 90% by 2022.

After realizing the possibilities for working alongside banks, they intended to increase their products and give customers better experiences. Over time, as regulatory environments evolved and financial institutions embraced partnerships, the BaaS model gained significant traction.

This fruitful collaboration empowers greater agility and innovation in the financial services space, benefiting consumers and businesses alike with an array of cutting-edge options and streamlined experiences.

Banking as a Service Examples

Through collaborating with banks, BaaS providers can concentrate on developing user-friendly interfaces and distinctive financial solutions while the banks efficiently handle the challenging back-end tasks and guarantee compliance.

Here are examples of banking as a service:

Online Banking

BaaS allows fintech and non-fintech companies to offer online banking services to their customers by integrating with a bank’s systems through APIs.

This integration enables businesses to improve user interfaces and create user-friendly apps while the bank handles the core banking functionalities.

Customers can conveniently track transactions, check account balances, and manage savings through third-party applications. The deep integration between banks and non-bank entities streamlines the user experience and enhances financial accessibility.

However, it requires robust security measures and compliance with regulations to safeguard customer data and ensure a seamless and trustworthy banking experience.

Debit and Credit Cards

Non-bank companies can leverage BaaS to provide credit and debit cards to their customers. This allows users to make purchases and transactions seamlessly while receiving real-time updates on their spending.

Additionally, attractive offers like cashback without expiry increase customer satisfaction and loyalty. Through BaaS, companies can issue branded cards that align with their business objectives and branding.

However, they must ensure transparent fee structures, competitive interest rates, and clear terms and conditions to maintain trust and customer retention.

Businesses can offer one-click loans or buy now, pay later options to their customers by integrating with banks through BaaS. This enables users to access flexible loan options for travel plans or purchase products and services without immediate full payment.

The model allows companies to streamline the loan application process and provide instant approvals, making it convenient for users.

However, responsible lending practices, clear disclosure of interest rates and terms, and efficient repayment tracking are essential to prevent overindebtedness and foster positive customer experiences.

Investment Services

Fintech and non-bank players use BaaS to offer their customers investment services. They are helping users automate finances, invest in low-cost index funds, and provide personalized investment plans based on individual risk profiles and financial goals.

Companies now get to democratize access to financial markets and foster financial literacy by integrating investment services with BaaS. To earn and keep the trust of their user base, they must prioritize data protection, give clear cost structures, and offer proper risk disclosures.

Customer Identification Verification

BaaS platforms assist businesses in verifying beneficiary bank accounts before payment transfers. This helps reduce payment failures and mitigates potential risks for organizations.

Integrating BaaS for verification processes streamlines payment workflows and enhances operational efficiency.

Data privacy and compliance with anti-money laundering(AML) and know-your-customer (KYC) regulations are critical considerations to prevent fraudulent activities and safeguard sensitive information.

BaaS enables non-bank companies to integrate P2P payment functionality into their applications. Users can send and receive money instantly to and from friends, family, or other users within the same platform.

P2P payments via BaaS enhance user convenience and encourage digital transactions. To ensure security, companies must implement robust authentication measures and fraud prevention mechanisms to protect user funds and maintain platform integrity.

Below is an example of a P2P crypto exchange. Several crypto exchanges, such as Binance, OKX, Huion,etc., are available in the market.

P2P crypto exchange – Image Source: Techopedia

Personal Finance Management

BaaS empowers businesses to offer personalized financial management tools and services to customers. These platforms can analyze users’ financial data, categorize expenses, create budgets, and offer advice based on individual spending patterns.

BaaS-powered personal finance management tools provide users with valuable insights into their financial health and help them make informed decisions.

Companies must prioritize data protection, transparency, and personalized recommendations based on users’ best interests to foster user trust.

Benefits of Baas

There are many advantages of using BaaS to power digital applications and websites. Let’s examine them:

Financial Inclusion

Banking as a Service (BaaS) promotes financial inclusion by enabling easier access to financial services for underserved populations.

Many individuals, especially in developing regions, may not have access to traditional banking services due to geographical limitations, lack of infrastructure, or inadequate financial history.

BaaS allows fintech companies and other businesses to integrate banking services into their platforms, making it possible to offer banking products and services to these underserved populations.

For example, a fintech company could use BaaS to provide a mobile banking app that allows people in remote areas to open digital bank accounts, conduct transactions, and access basic financial services without visiting a bank branch physically.

Innovation

It fosters innovation in the financial industry by allowing fintech companies and startups to build new financial products on existing banking infrastructure. This significantly reduces the time to market for novel solutions, as they can leverage the infrastructure and capabilities of established banks.

A good scenario is when a startup focused on peer-to-peer lending could use BaaS to quickly launch its platform by integrating with a partner bank’s lending services, eliminating the need to build the entire lending infrastructure from scratch.

Customer-Centric Solutions

The model empowers businesses to offer tailored customer experiences by choosing specific banking services to integrate into their platforms. This flexibility allows companies to enhance customer satisfaction by providing services aligned with their target audience’s needs.

Amazon is an eCommerce company that uses BaaS to integrate banking services like digital wallets and payment processing. It offers customers a seamless checkout experience and rewards programs directly through their mobile app.

Cost Savings

BaaS reduces costs for both banks and businesses by eliminating the need to build and maintain separate banking infrastructures.

For banks, it means they can extend their services to new markets without the need for physical branches. For businesses, it reduces the upfront investment and ongoing expenses associated with creating their banking infrastructure.

If you are a small fintech startup, it is good to leverage BaaS to provide checking and savings account services without investing in building and managing the entire backend banking infrastructure.

Scalability

It enables seamless scalability for businesses, allowing them to expand their offerings rapidly without extensive setup processes. This is particularly beneficial for fintech companies that experience rapid growth and need to accommodate a growing user base.

A peer-to-peer payment app can easily scale operations and handle increasing transaction volumes using BaaS providers’ scalable infrastructure.

Regulatory Compliance

BaaS providers leverage the regulatory expertise of established banks to ensure compliance with financial laws and regulations. Partnering with banks allows fintech companies and startups to navigate the complex regulatory landscape, reducing non-compliance risk.

For example, a cryptocurrency exchange can partner with a traditional bank through BaaS to ensure its operations comply with relevant anti-money laundering (AML) and Know Your Customer (KYC) regulations.

Partnerships

Banking as a Service fosters partnerships between traditional banks and tech companies, promoting collaboration and driving mutual growth in the financial industry. It enables banks to tap into the innovation and agility of fintech startups, while fintech companies can leverage the banks’ stability and customer base.

Some well-established banks partner with robo-advisory platforms through BaaS to offer its customers access to automated investment services and expand its range of financial offerings.

Challenges

While BaaS offers numerous benefits, it also comes with some challenges. Here are a few common ones

Outdated Core Systems

Some traditional banks struggle to integrate with modern technologies and third-party services because their core systems are outdated. These legacy systems were designed decades ago and lacked the flexibility for seamless integration.

As a result, banks face challenges in adopting innovative solutions and providing customers with the latest tech-driven services.

Data Security and Privacy Concerns

Implementing Banking-as-a-Service (BaaS) and increased data sharing between financial institutions and third-party players can raise data security and privacy concerns.

With more parties involved in handling sensitive financial data, the risk of data breaches and unauthorized access may escalate. Robust security measures and strict privacy protocols are crucial to safeguard customer information and maintain trust in the financial ecosystem.

Modern financial institutions are addressing these challenges by transitioning toward data-driven banking approaches that incorporate advanced encryption, real-time monitoring, and AI-powered anomaly detection systems. These sophisticated solutions enable banks to securely share information with third-party providers while maintaining granular control over data access and establishing comprehensive audit trails that track every interaction with sensitive customer information.

Well-Defined API Strategy

Opening up a bank through APIs presents a complex challenge as it demands a well-defined strategy for seamless integration with third-party services.

Banks must design APIs that cater to diverse use cases while ensuring security, scalability, and compliance with industry standards.

Creating a cohesive API ecosystem that meets the needs of external developers and promotes innovation while safeguarding customer data can be daunting.

Performance Issues

As the app’s backend is hosted on a shared infrastructure, performance can be affected by other apps using the same resources, leading to potential latency and response time challenges.

Cost Considerations

Banking as a Service (BaaS) can reduce upfront costs by outsourcing backend infrastructure. However, businesses should be cautious of recurring expenses, like transaction fees and licensing charges, which can accumulate over time.

For long-term projects, these costs may become significant factors to consider, affecting the overall financial viability of utilizing BaaS solutions. Proper cost analysis and comparison with in-house options are essential for making informed decisions.

Reliability and Uptime

By relying on a third-party BaaS provider for the backend, the app’s availability becomes dependent on the provider’s uptime and reliability.

Any service disruptions or downtime from the BaaS provider could directly impact the user experience, leading to potential inconvenience and frustration for app users.

Ensuring a reliable and robust BaaS provider becomes crucial to maintain a seamless and uninterrupted user experience.

The rise of Banking-as-a-Service (BaaS) can be attributed to several factors:

Customer Demand

The rise of Banking as a Service (BaaS) is driven by increasing customer demand for integrated financial services and user-friendly products.

Customers are seeking holistic experiences. BaaS allows businesses to create ecosystems where customers can access various financial services without using multiple providers.

Growth of the Fintech Industry

The expanding fintech industry relies on BaaS to offer financial products and services without the burden of obtaining a full banking license. BaaS provides a viable pathway for fintech companies to enter the market and collaborate with banks to deliver innovative solutions.

Regulatory Requirements

Open Banking initiatives in various countries have encouraged collaboration between banks and third-party providers.

Banks are required to make their APIs public, fostering competition and compelling traditional banks to adopt the BaaS model to stay competitive and meet customer expectations.

Serving the Unbanked and Small Businesses

BaaS enables banks to reach previously underserved segments, such as the unbanked and small businesses. Fintech players targeting these customer groups offer user-friendly online banking services and affordable loans. This leads traditional banks to collaborate with private financial institutions through BaaS to cater to these customer needs.

Banking Revenue

Integrating with non-banks through partnerships, such as the BaaS model, presents an opportunity for traditional banks to explore new streams of revenue and product growth.

By collaborating with businesses that possess highly scalable business models, banks can tap into the tech-savvy customer base of these partners, expanding their reach and serving more customers.

This strategic collaboration with non-banks can help traditional banks adapt to the changing landscape, especially with the potential decline in banking revenue and profitability.

Embracing innovation and catering to the demands of a digital-savvy customer base will be crucial for banks to remain competitive and sustain profitability in the evolving financial industry.

The future of Banking-as-a-Service (BaaS)

The future of BaaS looks promising and will likely continue growing and evolving in the financial industry. Here are some key aspects of the future of BaaS:

Expansion and Adoption

BaaS is expected to see increased adoption among financial institutions and non-banking companies. As more businesses recognize the benefits of BaaS, it will become a mainstream model for offering financial products and services.

Continued Technological Advancements

Advancements in technology will further enhance the capabilities of BaaS. Improved APIs, secure data sharing, and real-time integration between banking systems and third-party providers will become more sophisticated and reliable.

Global Expansion

BaaS is expanding globally, breaking geographical barriers, and offering financial services seamlessly across borders. This facilitates cross-border transactions and international business operations.

Banking as a Service (BaaS) represents a transformative shift in the financial industry, enabling non-bank entities to integrate essential banking functionalities into their platforms through APIs.

BaaS offers numerous benefits, including promoting financial inclusion by extending services to underserved populations and fostering innovation by allowing startups to build new financial products on existing banking infrastructure.

It empowers businesses to provide customer-centric solutions tailored to their target audience’s needs while reducing costs and ensuring scalability. Despite its advantages, BaaS has challenges, such as outdated core systems, data security and privacy concerns, and well-defined API strategies.

The rise of BaaS can be attributed to factors like increasing customer demand for integrated financial services, the growth of the fintech industry, and regulatory requirements promoting collaboration between banks and third-party providers.

The future of BaaS looks promising, with continued expansion, technological advancements, and global adoption expected. As BaaS continues to evolve, it will play a pivotal role in reshaping the financial landscape.

Acodez is a leading web development company in India offering all kinds of web design and development solutions at affordable prices. We are also an SEO and digital marketing agency offering inbound marketing solutions to take your business to the next level. For further information, please contact us today.

Looking for a good team

for your next project?

Contact us and we'll give you a preliminary free consultation on the web & mobile strategy that'd suit your needs best.

Rithesh Raghavan, Co-Founder, and Director at Acodez IT Solutions, who has a rich experience of 16+ years in IT & Digital Marketing. Between his busy schedule, whenever he finds the time he writes up his thoughts on the latest trends and developments in the world of IT and software development. All thanks to his master brain behind the gleaming success of Acodez.