The role of smartphones has grown beyond communication. One clear shift is how payments are made. More people now depend on mobile apps to pay safely and fast, without using cash.

The use of these apps keeps growing each year. They’re helping move the world toward a more cashless way of living. Digital payments are no longer optional for businesses. Customers now see them as a standard part of any service.

It’s almost impossible to imagine life without our phones now. Mobile wallets, contactless payments, and QR code options aren’t just trends anymore – they’ve become part of everyday transactions.

Since the pandemic, many businesses have leaned further into digital payments. Contactless systems are now the norm, as people prefer quick and touch-free ways to pay instead of using cash.

The proliferation of mobile payment apps, already commonplace on our cell phones, may be more apparent than ever.

In this article, we’ll examine the evolution of mobile payment solutions, their integration in apps, and how they’re advancing the cashless society.

Digital payments have gained acceptance as a legitimate means of conducting business because of the rising popularity ofe-commerce.Even more, stores are integrating mobile payment applications with their point-of-sale (POS) systems.

Mobile wallets, also known as digital wallets, let people make payments right from their phones. They keep your card or bank details stored safely, so you don’t have to type them every time you buy something.

Most of these apps work with simple tech like Near Field Communication (NFC), Quick Response (QR) codes, or your fingerprint and face ID to finish payments fast and safely. You can also move money between accounts using your phone or tablet.

This method started gaining attention in Asia and Europe before it became common in North America.

To accept mobile payments, PayPal and Apple Pay introduced a barcode in 2014 that could be read by a store’s barcode scanner. A contactless credit card terminal was tapped by mobile devices to collect payments as a result of later improvements.

Some believe this contactless payment technique can effectively replace actual debit or credit cards. Compared to more conventional payment options, it is quicker, more trustworthy, and more secure.

Users can effectively complete transactions from a mobile device with mobile payments. Some mobile payments use third-party apps to conduct transactions, while others use a mobile wallet saved on the smartphone.

Mobile wallets and mobile money transfers are the two primary methods for making mobile payments. In other words, the evolution of mobile payment solutions has enabled customers to pay for goods and services online rather than with cash or credit cards.

The Evolution of Mobile Payment Solutions

The use of mobile payment apps has grown significantly in recent years. Humans have always relied on a payment system to get the commodities or services we wanted or needed.

Humans used animals, grain, shells, metal coins, pieces of white deerskin, wampum, gold, the dollar backed by gold, charge cards, credit cards, the U.S. dollar, and, most recently, computerized payments after starting with the bartering system.

We like simple and transactional payments, if there has been one recurring pattern in the evolution of payments. With the invention of the charge card at the turn of the 20th century, these preferences started to take shape.

Although Edward Bellamy initially mentioned them in his 1887 novel “Looking Backward,” the first credit card wasn’t provided to users of Western Union until 1921.

Soon after, department stores, gas stations, and motels made charge cards available to clients, saving them the trip to their local bank. After the Diners Club card was introduced in 1950, the credit card market started to resemble what we are accustomed to today. The first credit card of the contemporary era, issued by a third-party bank, was the BankAmericard, established in 1958. In 1977, the card was renamed Visa.

Since then, technology has given us the late 1970s/early 1980s videotex systems, online bill payment and banking in 1994, mobile web payments (WAP) in 1997, and the wave of mobile payment apps we are currently using.

The convergence of technological advances, improved connectivity, and changing user expectations has led to the widespread usage of mobile apps.

The industry for digital payments is expected to reach $25 trillion in transaction value by 2027, demonstrating the significant growth and expanding importance of the evolution of mobile payment solutions within the financial ecosystem. The global mobile payment market was valued at USD 3.84 trillion in 2024 and is projected to grow to USD 4.97 trillion in 2025

The Integration of Mobile Payment Solutions

The evolution of mobile payment solutions has made various financial services more broadly accessible.

In a PwC survey, 86% of respondents said that partnerships between traditional banking companies and fintech and digital startups will serve as the primary source of innovation.

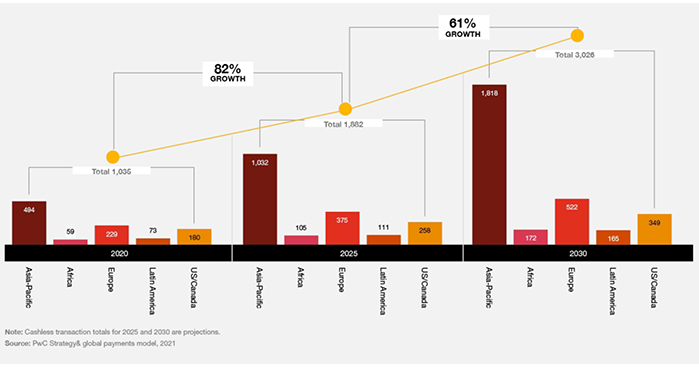

Statistics of Cashless Transaction Volume – Image Source: PwC

The prevalence of cashless transactions is expected to increase by 2030, so they may very well become the norm. Below are some of the trends that show their integration in apps.

Super Apps

Super applications, which provide a variety of services on a single platform, have grown significantly with the evolution of mobile payment solutions in many places.

Numerous features, including texting, e-commerce, ride-hailing, food delivery, and financial services, including payments, are integrated into these apps.

Super applications make users’ lives easier and give them a unified experience, but they also present problems for stand-alone mobile payment apps. Super apps can take over the market by providing integrated payment services in addition to their core features.

Stand-alone payment apps struggle to compete effectively against their large user bases and established infrastructure. Additionally, they can manage enormous volumes of consumer data across numerous services.

Users who may be reluctant to provide critical financial information within these integrated platforms may have worries about the complexity of ensuring sufficient security measures and protecting user privacy.

The simplicity of usage of mobile wallets is primarily responsible for their popularity. Users merely need to provide their bank account information and download a mobile app. After identity verification, consumers can immediately make transactions online or in person.

Mobile wallets enable contactless payments using mobile payment apps by utilizing near-field communication (NFC), a technology that enables data to be transmitted over relatively small distances.

Peer-to-Peer Payments

Soon, peer-to-peer (P2P) transactions will probably skyrocket. In 2025, mobile P2P payments are expected to reach more than $1 trillion in transaction volume, according to Cognitive Market Research. P2P transactions are an important part of the development of the mobile payment ecosystem, even though they don’t always involve merchant partnerships.

P2P payments allow customers to enjoy quicker and more seamless transactions between two or more persons via mobile apps.

P2P is a favorite payment option for younger generations because of its security and ease. Users only need to enter a phone number or email address to send money while keeping their bank information confidential.

You can move money directly between two people using peer-to-peer payment techniques without using a middleman. Suppose you attend a party, your friend covers the cost, and you subsequently have to reimburse her. How do you behave? Open an app, enter money, and then pay. SIMPLE!

Buy Now Pay Later

Embedded lending is the incorporation of loan services into the transaction flow, whereas BNPL enables customers to postpone making payments on their purchases.

Due to their ease and flexibility for clients, these payment solutions are growing in popularity. Previously, retailers would offer special deals like “buy now, pay later” (BNPL) to persuade customers to purchase. But more lately, it has developed into a staple service.

Similar to credit cards, this method of financing allows you to bypass credit checks, cheaper interest rates, and other expenses. BNPL enables customers to make an urgent purchase and postpone payment until more money is available.

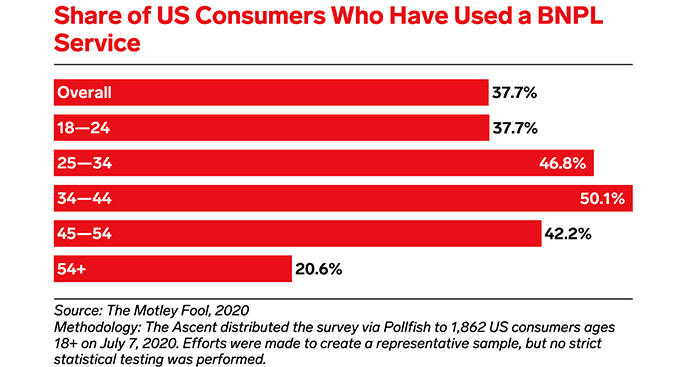

According to Insider Intelligence, Gen Z and Millennials are the target demographic for the BNPL payment mechanism.

Statistics of Consumers Who Have Used a BNPL Service – Image Source: Insider Intelligence

But it’s also popular across a range of age groups. Adoption keeps growing as more individuals become aware of how this payment method functions. According to a poll, 62% of BNPL customers think the system might eventually replace credit cards.

BNPL services are becoming increasingly popular across the world. A Juniper Research report predicts that more than 900 million people will use BNPL platforms by 2027.

Cryptocurrency

As online businesses started going global, sending money across borders became a bit of a headache, with slow transfers, high fees, and a lot of waiting around. That’s whencryptocurrenciesentered the scene, promising faster and cheaper payments without the usual middlemen.

Instead of relying on banks, crypto runs on blockchain, a transparent digital network where money moves directly between people. It sounded like the perfect fix for expensive international payments, and for a while, it really was making waves.

But after the wild crypto swings of 2022–2023 and tighter government rules, many companies became more cautious. Even so, crypto’s biggest contribution wasn’t just the currency itself; it was the idea behind it. The technology pushed the entire payment industry to innovate.

Today, we’re seeing that influence in stablecoins and Central Bank Digital Currencies (CBDCs), both built on the same blockchain principles but designed for stability and trust. So even if crypto didn’t take over payments entirely, it definitely changed the game for good.

Cryptocurrencies don’t need intermediaries because they are powered byblockchain technology. As a result, transaction costs are effectively reduced, enabling transfers to occur instantly. Customers only need to see the merchant’s public Bitcoin wallet address.

AI- Secured Payments

Digital payment providers use machine learning and AI algorithms to strengthen the security of transactions. These are mostly employed to raise security by spotting odd behaviors or transactions.

It is not surprising to see hackers target mobile payment customers, given the expanding popularity of mobile payments.

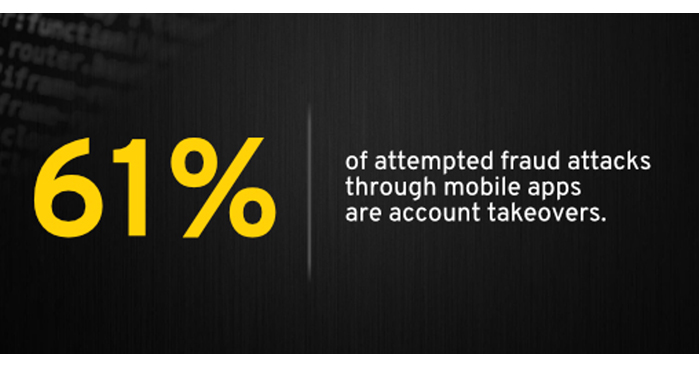

According to a NICE Actimize analysis, account takeovers comprise 61% of attempted mobile payment fraud assaults. Artificial intelligence (AI) can help with this.

Percentage of Attempted Fraud Attacks Through Mobile Apps – Image Source: Help Net Security

Financial services can spot odd activity through transaction filtering and prevent questionable transactions.

Real-time consumer variables, such as purchasing patterns, biometrics, and geolocation, can be used by AI technology and machine learning capabilities to stop fraudulent transactions. Fraud detection gets more precise with AI and ML.

These systems assist in decreasing the number of false positives in fraud detection since they can understand data. The capacity of these systems to learn over time is essential for spotting previously undiscovered strategies employed by evildoers.

MPOS Technology

Mobile point-of-sale (mPOS) technology has grown in popularity with the introduction of mobile payments. As a result, systems for processing credit card payments are now also portable.

These gadgets have a unique wireless system that enables them to perform the same functions as standard sales terminals and cash registers.

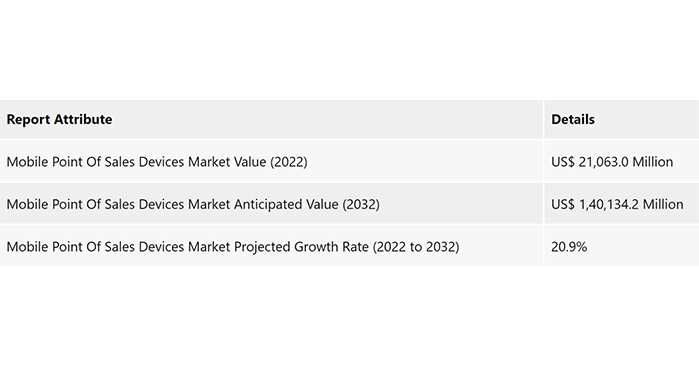

According to research by Future Market Insights, the mPOS market would develop at a compound annual growth rate (CAGR) of 20.9 percent from 2022 to 2032, reaching $140.2 billion in the upcoming years.

Statistics of mPOS Market – Image Source: Future Market Insights

This rise is primarily due to the adaptability of mPOS technology, which can be used at food trucks, trade shows, concerts, fairs, and mobile shops in addition to traditional retail locations.

Contactless Credit Cards

Credit cards already provide quick and safe purchases, but contactless cards further increase these advantages. A credit card with a chip is tapped over a payment terminal to complete the transaction, and NFC is utilized to transfer data wirelessly.

The payment system creates a code using this technology that is unique to a credit card and the transaction being processed. Because only the bank can decode it and validate the transaction, this one-time-use code adds extra protection.

Examples of Payment Gateways

There are several payment gateway systems available right now that have both strong and poor points. For instance, some offer support for over a hundred different currencies, some concentrate on cryptocurrencies or even accept them, while some add more security measures.

Since everything relies on your company’s requirements, you should establish your objectives, determine your budget, research the many mobile app payment gateways, and select the ideal one.

Below are some of the most well-liked payment processors;

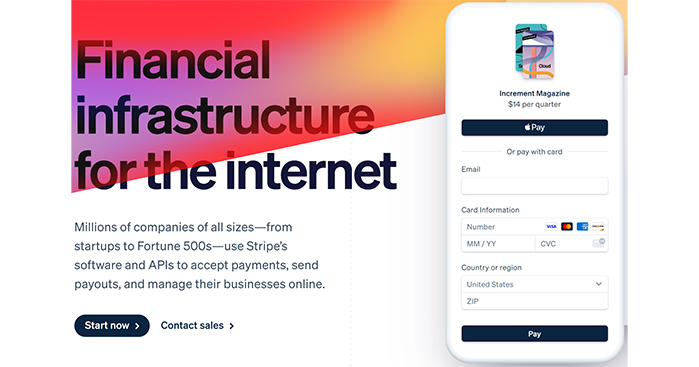

Stripe

Stripe Payment Gateway – Image Source: Stripe

The payment gateway provider Stripe is situated in San Francisco, and their software makes it simple for businesses and individuals to send money. This payment gateway solution provides online payment systems’ technological and financial underpinning.

The service continuously scans the network for suspicious activity to guarantee secure data storage and avoid fraud.

With support for debit and credit cards, Apple Pay, Android Pay, Bitcoin, and Amex Express Checkout, Stripe is currently used in more than 100 countries. Its well-known clients are Lyft, Instacart, Postmates, DoorDash, TaskRabbit, and Grab.

The usual commission rate offered by Stripe is 2.9% of each financial transaction + $0.3 for money transfers. Additionally, it eliminates all fees for foreign payments and offers some savings to companies with monthly revenues of $80,000 or more.

Paypal

One of the innovative businesses that once set the bar in its industry was PayPal. As for now, this payment gateway provider is still very well-liked for the factors that helped it establish itself as a leader in its early years: simplicity, security, and global reach.

Virtually any country’s citizens can purchase and place service orders online without providing their credit card information.

Braintree

The Chicago-based business Braintree specializes in providing digital finance solutions for the eCommerce sector. It was bought by PayPal in 2013, and the Braintree SDK now allows for integration.

This payment gateway option is a fantastic option for small and mid-sized businesses. Similar to Stripe, Braintree charges a standard cost of2.9% of each operation plus 30 cents per transaction and accepts the first $50,000 in payments free of charge.

Square

Square Payment Gateway – Image Source: Square

Square is a financial services firm that also offers mobile payments. Among other things, Square’s payment gateway enables retailers to take payments via mobile apps.

They provide a complete solution with the payment gateway, merchant account, and secure payment APIs already built in.

Benefits of Mobile Payment Systems

In comparison to conventional payment methods, the evolution of mobile payment solutions has brought about several benefits. Mobile payment options are a significant addition to any payment strategy since they provide businesses and customers with many benefits.

The following are the main advantages of utilizing mobile payment options:

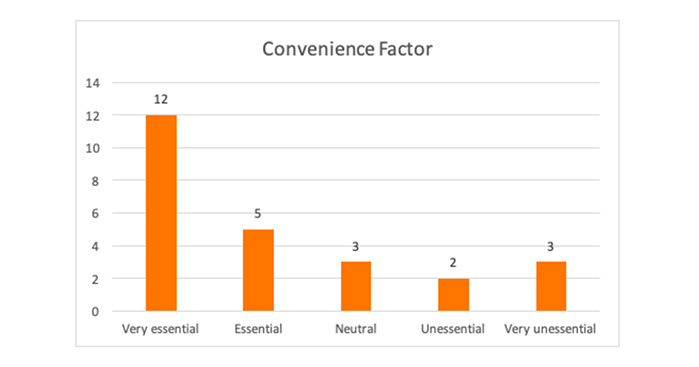

Convenience

Thanks to mobile payment solutions, users may pay for goods and services using their mobile devices whenever and wherever they choose. Mobile payments make transactions quicker and simpler by eliminating the need to carry cash or credit cards.

Importance of Mobile Payments Convenience – Image Source: KTH

Security

Due to their cutting-edge encryption and other security features to safeguard customers’ financial information, mobile payment systems are typically more secure than traditional payment methods. Fraud, identity theft, and other security breaches are less likely.

Speed

Mobile payment solutions enable consumers to make transactions quickly and simply without physical payment methods. It makes the waiting time short for both customers and retailers during checkout.

Accessibility

Due to the lack of a bank account or credit card requirement, mobile payment solutions are more widely available to consumers than traditional payment methods. The underbanked or unbanked can now more easily engage in the digital economy.

Cost-Effectiveness

Due to the absence of physical payment processing infrastructure and other related expenses, mobile payment solutions are frequently less expensive than traditional payment methods.

By doing this, businesses can cut costs on transaction fees and other expenses, which may result in lower customer prices.

Integration

Mobile payment options are simple to interface with other technologies and systems, such as restaurant inventory and accounting software, to help these firms better run their operations.

Future trends in mobile payments are interesting. The evolution of mobile payment solutions as a transformative force has hastened the transition to a cashless society by changing how we conduct financial transactions.

The ease of use, accessibility, improved security, and data-driven personalization of mobile payment applications have increased their appeal among customers and companies.

Stakeholders must address privacy issues, ensure interoperability, and promote financial literacy as these apps develop to fully benefit from mobile payment applications in promoting financial inclusion, economic growth, and a seamless cashless experience.

The future of mobile payments is undoubtedly 100% mobile, and at Reloadly, we are thrilled to be a part of this transformation. The mobile payments sector is flooded with opportunities.

Acodez is a leading web development company in India offering all kinds of web design and development solutions at affordable prices. We are also an SEO and digital marketing agency offering inbound marketing solutions to take your business to the next level. For further information, please contact us today.

Frequently Asked Question

How secure are mobile payment apps really, and should I trust them?

Mobile payment apps like Apple Pay and Google Pay use tokenization, encryption, and biometric login, making them very secure—often safer than using a physical card. Most risks come from weak phone security or malware, not the payment apps themselves. As long as your device is protected, they’re generally trustworthy.

Why do some merchants still refuse mobile payments?

Many small merchants avoid mobile payments due to perceived higher fees, lack of technical knowledge, or not realizing their existing terminals already support NFC. Some are also hesitant due to habit or concerns about reliability. Adoption is improving but still slower in smaller towns and rural areas.

Is cryptocurrency practical for everyday shopping?

Crypto payments aren’t practical for most retail because of price volatility, slow transaction speeds, and unclear regulations. Stablecoins work better for business transfers, but everyday consumer payments using crypto remain niche.

Looking for a good team

for your next project?

Contact us and we'll give you a preliminary free consultation on the web & mobile strategy that'd suit your needs best.

Jamsheer K, is the Tech Lead at Acodez. With his rich and hands-on experience in various technologies, his writing normally comes from his research and experience in mobile & web application development niche.

I completely agree with you on moving towards digital transformation.

I personally think mobile wallets will be the future of payment processing